April 1, 2013 Bankruptcy Dollar Adjustments: What to Expect

The bankruptcy code at 11 USC 104 provides for the periodic adjustments of certain dollar figures in the bankruptcy code every 3 years to account for inflation. The next set of new figures will be effective April 1, 2013. Closer to that date, the courts will publish an official list of changes. However, the Consumer Price Index data needed for the adjustment is now available, so it is possible to predict what these adjustments will be.

Based on my review of the CPI data, I believe the inflator value of 1.063 will be applicable to the Section 104 calculations. This is somewhat more modest then the 1.070 inflator of 2010 and 1.095 inflator of 2007, but is to be expected given the economic conditions of late.

Once an inflator is determined, the dollar adjustments can be calculated. I'll start by discussing a few that I believe are particularly relevant, and then at the end include a table of predicted changes. While a 6.3% increase is not particularly large, the numbers to be adjusted are occasionally very consequential in bankruptcy cases. Debtors on the margin might find a small change very significant.

Please note that the numbers in this post are the product of one attorney's predicted calculation, and should not be used in place of the official numbers, which will be released in coming weeks.

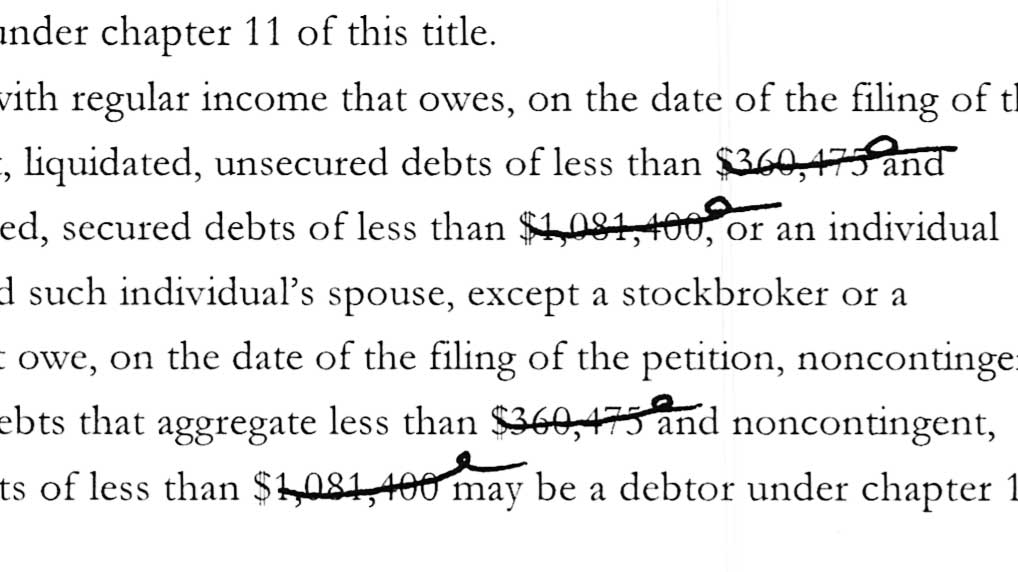

1. Chapter 13 Debt Limit Increases

Section 109(e) of the bankruptcy code limits the eligibility of people to file chapter 13 bankruptcy based on amount of debt. Based on the predicted inflation value, the limit on noncontingent liquidated unsecured debt would increase from $360,475 to $383,175, and the limit on noncontingent liquidated secured debt would increase from $1,081,400 to $1,149,525. The debt limits come up with some frequency, and at times are a harsh cut-off from cost-effective reorganization under chapter 13.

2. Means Testing Thresholds

The means test controls chapter 7 eligibility by providing a grounds to dismiss chapter 7 cases that fail the test and are "presumed abusive." In chapter 7, a case is "presumed abusive" if, after applying statutorily allowed deductions, too much income remains. Whether or not the income after deductions is too much is determined by comparison to two statutory thresholds, both of which are scheduled to be increased by the April 1 adjustments.

Based on my calculations, one threshold would increase from $11,725 to $12,475 and the other from $7,025 to $7,425. For debtors with at least $50,000 in unsecured debt, this amounts to a increase in $12.50 per month in income that would not trigger means testing eligibility issues. Practically speaking, such a fairly modest change and not any more consequential than the semi-annual means testing adjustments.

The means test only applies if a debtor is above the median income for his or her household size. While household sizes of 1 to 4 use actual statistical data, households "medians" for household sizes of 5 and more are calculated by adding a statutory amount to the UST published statistic for a household of four. This monthly statutory figure is likely to increase from $625 to $675. The consequence is that annual medians for households of 5 would increase by $600; households of 6 by $1,200, households of 7 by $1,800, and so forth.

3. Bankruptcy Code Exemptions

Section 522(d) creates the so-called "federal exemptions" which certain debtors claim to protect their assets in bankruptcy. Some states allow their residents to choose the federal exemptions, while others, including North Carolina, do not. Most NC residents will use the NC statutory exemptions, not the 522(d) federal exemptions. The exception is certain cases where the debtor has moved to North Carolina from particular states within the two years prior to filing the bankruptcy case.

Many of the 522(d) federal exemptions are limited to a certain dollar amount of property. Each of these limits will increase on April 1, 2013 with the inflation adjustment. Applying my 6.3% estimate, changes would include an increase in the homestead exemption from $21,625 to $22,975 and the motor vehicle exemption from $3,450 to $3,675, for example (see also full table below).

4. Fraudulent Debt Presumptions

If a creditor proves a particular debt was obtained by false pretenses or fraud in a dischargability adversary proceeding, the debt is not discharged and survives the bankruptcy. The creditor has an easier case when one of two situations exist and fraud is presumed: (1) purchases of luxury goods totaling more than $600 in the 90 days prior to bankruptcy and (2) certain cash advances totaling $875 in the 70 days prior to bankruptcy. Both of these figures will be adjusted, to $650 and $925 respectively based on my predictions.

Full Table

The below table reflects my calculations based on Section 104 and a predicted 1.063 inflator:

| 2010 | Predicted 2013 | |

|---|---|---|

| Section 101(3) - definition of assisted person | $175,750 | $186,825 |

| Section 101(18) - definition of family farmer | $3,792,650 | $4,031,575 |

| 101(19A) - definition of family fisherman | $1,757,475 | $1,868,200 |

| 101(51D) - definition of small business debtor | $2,343,300 | $2,490,925 |

| Section 109(e) - allowable debt limits for individual filing bankruptcy under chapter 13 | $360,475 | $383,175 |

| $1,081,400 | $1,149,525 | |

| Section 303(b) - minimum aggregate claims needed for the commencement of involuntary chapter 7 or chapter 11 bankruptcy | ||

| (1) - in paragraph (1) | $14,425 | $15,325 |

| (2) - in paragraph (2) | $14,425 | $15,325 |

| Section 507(a) - priority expenses and claims | ||

| (1) - in paragraph (4) | $11,725 | $12,475 |

| (2) - in paragraph (5) | $11,725 | $12,475 |

| (3) - in paragraph (6) | $5,775 | $6,150 |

| (4) - in paragraph (7) | $2,600 | $2,775 |

| Section 522(d) - value of property exemptions allowed to the debtor | ||

| (1) - in paragraph (1) | $21,625 | $22,975 |

| (2) - in paragraph (2) | $3,450 | $3,675 |

| (3) - in paragraph (3) | $550 | $575 |

| $11,525 | $12,250 | |

| (4) - in paragraph (4) | $1,450 | $1,550 |

| (5) - in paragraph (5) | $1,150 | $1,225 |

| $10,825 | $11,500 | |

| (6) - in paragraph (6) | $2,175 | $2,300 |

| (7) - in paragraph (8) | $11,525 | $12,250 |

| (8) - in paragraph (11)(D) | $21,625 | $22,975 |

| 522(f)(3) - exception to lien avoidance under certain state laws | $5,850 | $6,225 |

| 522(f)(4)- items excluded from definition of household goods for lien avoidance purposes | $600 | $650 |

| 522(n) - maximum aggregate value of assets in individual retirement accounts exempted | $1,171,650 | $1,245,475 |

| 522(p) - qualified homestead exemption | $146,450 | $155,675 |

| 522(q) - state homestead exemption | $146,450 | $155,675 |

| 523(a)(2)(C) - exceptions to discharge | ||

| in subclause (i)(I) - consumer debts, incurred | $600 | $650 |

| in subclause (i)(II) - cash advances incurred | $875 | $925 |

| 541(b)- property of the estate exclusions | ||

| (1) - in paragraph (5)(C) - education IRA funds in the aggregate | $5,850 | $6,225 |

| (2) - in paragraph (6)(C) - pre- purchased tuition credits in the aggregate | $5,850 | $6,225 |

| 547(c)(9) - preferences, trustee may not avoid a transfer if, in a case filed by a debtor whose debts are not primarily consumer debts, the aggregate value of property is less than | $5,850 | $6,225 |

| 707(b) - dismissal of a case or conversion to a case under chapter 11 or 13 (means test) | ||

| (1) - in paragraph (2)(A)(i)(I) | $7,025 | $7,475 |

| (2) - in paragraph (2)(A)(i)(II) | $11,725 | $12,475 |

| (3) - in paragraph (2)(A)(ii)(IV) | $1,775 | $1,875 |

| (4) - in paragraph (2)(B)(iv)(I) | $7,025 | $7,475 |

| (5) - in paragraph (2)(B)(iv)(II) | $11,725 | $12,475 |

| (6) - in paragraph (5)(B) | $1,175 | $1,250 |

| (7) - in paragraph 6(C) | $625 | $675 |

| (8) - in paragraph 7(A) | $625 | $675 |

| 1322(d) - contents of chapter 13 plan, monthly income | $625 | $675 |

| 1325(b) - chapter 13 confirmation of plan, disposable income | $625 | $675 |

| 1326(b)(3) - payments to former chapter 7 trustee | $25 | $25 |

| 28 USC 1409(b) - a trustee may commence a proceeding arising in or related to a case to recover | ||

| (1) - money judgment of or property worth less than | $1,175 | $1,250 |

| (2) - a consumer debt less than | $17,575 | $18,675 |

| (3) - a non consumer debt against a non insider less than | $11,725 | $12,475 |

Update 2/21/2013: The official numbers have been posted to the federal register, and are as predicted in this post.

- Log in to post comments